Are you looking to finance a new construction project? Before your loan can be approved, your lender will need an appraisal for the home construction. Existing homes are usually easy to appraise because they can be compared to other homes. But how can a home be appraised before it’s even built?

The appraisal process for financing new construction can seem complicated at first, but as with everything else in this process, the steps you take are determined by how you’d like to finance the construction. Your lender is investing in your home, and if you cannot pay for it, they’ll need to sell it. Most lenders want to help you, but the venture may be risky for them if there aren’t many comparable homes in your area.

When planning the construction of a new home, you may want to know what can work against you during the appraisal process and how an appraiser will evaluate your home plans. You may end up reconsidering some of your home’s planned features or put in additional effort to find comparisons for your new home. If you’re feeling worried or overwhelmed with your construction loan appraisal process, we have the information you need to put your mind at ease.

- The Role of the Appraisal Process in Construction Financing

- How Long Does the Appraisal Process Take?

- Steps of the Appraisal Process

- Acquiring Specs and Cost Breakdown

- Estimating Home Value

- Analyzing Elements of Credibility

- Completing the Uniform Residential Appraisal Report

- Obtaining the Certificate of Completion

- Review Your Appraisal

- Make Upgrades or Changes

- Finance Your Construction Loan

- Underwriting for Construction Loans

- Closing

The Role of the Appraisal Process in Construction Financing

An appraisal is an opinion given by a licensed appraiser on the value of a property. The appraiser must follow set rules when appraising a property. The appraisal is just as important as your income, credit and assets when you’re applying for a construction loan. For new home construction, the appraisal is even more important than an appraisal for an existing home.

The two options here are if the builder will finance or if the buyer will finance. Usually, when the builder is the borrower, they:

- Own the lot already

- Don’t know who the future homeowner will be

If you’d like the builder to fund the construction, then a “subject to” appraisal will be performed at the time of the initial underwriting.

A “subject to” appraisal is where the value of the property is based off what the home will be worth in the future. It helps you evaluate the home after the improvements have been made. “Subject to” appraisals are a good way to make sure you don’t “over-improve” your home.

Appraisals are good for 120 days or 180 days for Veterans Affairs Loans (VA). If the house is not completed within this time, either a “Recertification of Value” or a new appraisal will be completed by the appraiser before the purchase is finished.

When the house is complete, the appraiser will provide a “Final Inspection” report. It’s important to note that if the builder finances the construction, the Loan-To-Value (LTV) is calculated by using the lesser of the purchase price or the appraisal.

The other side of the coin is if you, the buyer, will be financing the construction. Usually, when the homeowner is the borrower, they:

- Own the lot already

- Have a contract for construction with a builder

- Will use the loan funds to pay their builder

In this process, there are no drastic differences between this and builder financed. This appraisal process starts off with a “subject to” appraisal performed at the time of the initial underwriting. The appraisals are still good for 120 days or 180 days for VA loans.

If the house is not completed within this period, either the appraiser will complete a “Recertification of Value” or a new appraisal, although there is an exception for VA loans.

How Long Does the Appraisal Process Take?

So how long does a construction loan appraisal take? The appraisal itself can take two to four weeks or even longer if the area is farther away from where the appraisers work and live. Keep this general timeline in mind as you’re getting into the appraisal process.

Steps of the Appraisal Process

Construction loans are usually higher risk than loans for completed properties. Risks for construction loans include improvements not being completed, cost overruns, mechanic’s liens and faulty construction. To reduce their risk, lenders can:

- Control the disbursement of the loan funds

- Acquire title insurance endorsements before every disbursement

- Hold the contractor’s profit back

- Get lien releases

- Acquire completion and payment bonds

The lender’s goal is always to have enough funds to complete the construction. Because a loan for new home construction can present several risks for a lender, the appraisal plays a key role in determining whether the lender will approve a borrower for a loan and for how much. In many cases, an appraisal can even be the cause for loan denial.

So what exactly is the appraisal process for construction financing? Here are the steps, from construction loan pre-appraisal to certified completion.

1. Acquiring Specs and Cost Breakdown

Builders should keep a building plan for the home they are constructing and specifications that list the construction materials used. Builders will also keep a cost breakdown list for the labor of each home they build. The plot plan for a new construction home should show where it will be located on the site, along with where any accessory buildings will be located. Homebuilders will give mortgage lenders a home’s building plan, cost breakdown list, plot plan and spec sheets for an appraisal.

The more detailed and accurate spec sheets and home construction plans are, the more likely an appraiser can determine the level of finish and construction in your future home. An appraiser may discuss the home with the builder representative and even the borrower to confirm or get a better understanding of the drawings, spec sheets and level of finish on the new construction.

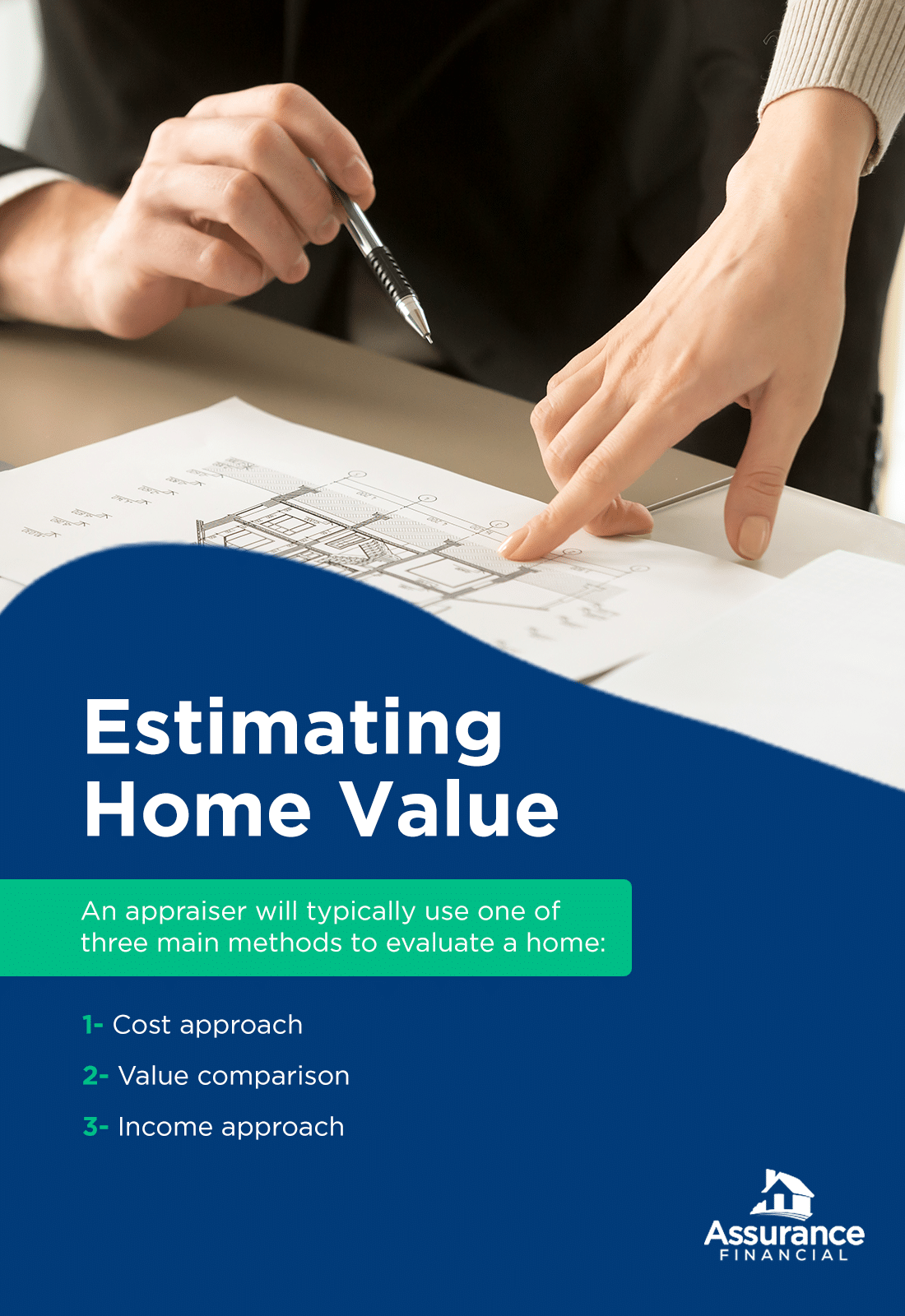

2. Estimating Home Value

An appraiser will typically use one of three main methods to evaluate a home:

- Cost approach: In the cost approach, the appraiser adds the cost of the land to the cost to reproduce or replace the house. This method can be inaccurate, however, because appraisers use a national database to determine costs, and materials can cost different amounts depending on where in the country you’re located.

- Value comparison: The value comparison approach estimates a home’s value by looking at the sale prices of similar homes nearby. This method is the most common, so finding comparable properties is essential. Because a new construction home can be unique for its location, though, there may be few comparable homes in the area.

- Income approach: This appraisal method isn’t very common, but it accounts for whether the home will be an income-producing property.

For a house to be comparable to your new home construction, it must typically be located a set limit of miles away and on a similar size of land. For urban areas, comps must be within half a mile or less but can sometimes be extended to a mile. For suburban areas, comps must be located within 1 to 3 miles. For rural areas, comps must be located within 5 to 10 miles.

A home can also only be considered a comp if it has sold on the open market in the last six months. Sometimes this can be extended to a year, but most lenders prefer comps that are six months old or less.

If you are planning to build a colonial-style home of 1,500 square feet on 3 acres of land, your appraiser must locate three other homes of approximately 1,500 feet on about 3 acres of land. If the appraiser can’t find at least three comparable homes, they could find it difficult to establish your new home’s value, leading to a possible loan denial or the lender lowering your loan amount.

Without sales in the immediate neighborhood, appraisers may expand their searches to nearby areas for homes that are similar, even sometimes exceeding the lender’s distance guidelines if necessary to acquire a credible value estimate. The appraiser will explain why a sale was used and any dollar adjustments that account for the differences in markets between the different locations.

Alternatively, an appraiser may also find a comparable older home within the same neighborhood as the new home construction. If this older home has similar square footage, finishes and overall utility, then a comparison can be made, adjusting for the differences in age, condition and depreciation.

The best approach you can take as the borrower is to know the area in which you are hoping to build a home. Some borrowers want to build homes that are much bigger and more expensive than other homes in the area, which is known as overbuilding. Though they may be qualified as a borrower, their loan could still be denied if the appraiser can’t establish a legal appraisal value. If you want to build on a lot of 20 acres in an area where most homes are built on 2 to 3 acres, you may also face issues with the appraisal. Lenders want to be able to sell a property quickly if necessary, but if a home is out of the ordinary for the area, they may not be able to do so, making the home construction a risky investment.

3. Analyzing Elements of Credibility

An appraisal must contain several key elements to be considered credible. The appraiser will identify the property they will be appraising and the total scope of the work they will be performing. Your home’s appraisal will list an estimated value and how this estimate was derived. The appraisal process requires appraisers to use certain forms to present their data and analysis clearly.

4. Completing the Uniform Residential Appraisal Report

Many home appraisers use this report. Fannie Mae developed the Uniform Residential Appraisal Report (URAR) to allow home appraisers to produce credible appraisals on both existing and new construction homes. Appraisers can combine this URAR with the estimated cost of the land and builders’ documents to determine home values for construction homes.

5. Obtaining the Certificate of Completion

Once all the needed improvements are made, the appraiser will return to verify the work. According to Fannie Mae, the certificate of completion must:

- Be completed by your home’s appraiser

- State improvements were completed and align with conditions and requirements from the initial appraisal report

These are the main steps involved in the appraisal process, but you aren’t ready to finance your new home construction just yet.

What’s Next After the Appraisal Process Is Complete?

When the house is complete, the appraiser will provide a “Final Inspection” report. The appraiser of the new construction home will send the appraisal to your mortgage lender to use when deciding on your loan. Here are some new construction appraisal guidelines to follow.

1. Review Your Appraisal

What if the appraisal is lower than what you expected? First, review the appraisal thoroughly. Check for issues in adjustments or missing features in the description of your planned improvements that the appraiser may have missed. If there are items you feel weren’t accounted for adequately in the appraisal, make a list.

You may also want to review the comparable sales included in the report. Double-check for factors that may have a negative influence on the comparable sale’s value that the appraiser may have overlooked and failed to account for, such as a school system. Check the gross living area, also known as the taxable living area, for each sale. You can find this information in the local tax record online. Make sure all of the data you find is congruent with what the appraiser has reported.

If you’ve found any significant errors or inconsistencies in the report after your close review, create a polite, thoughtful document to support your conclusions with facts and data and pass it on to the lender. You can request a second appraisal if necessary.

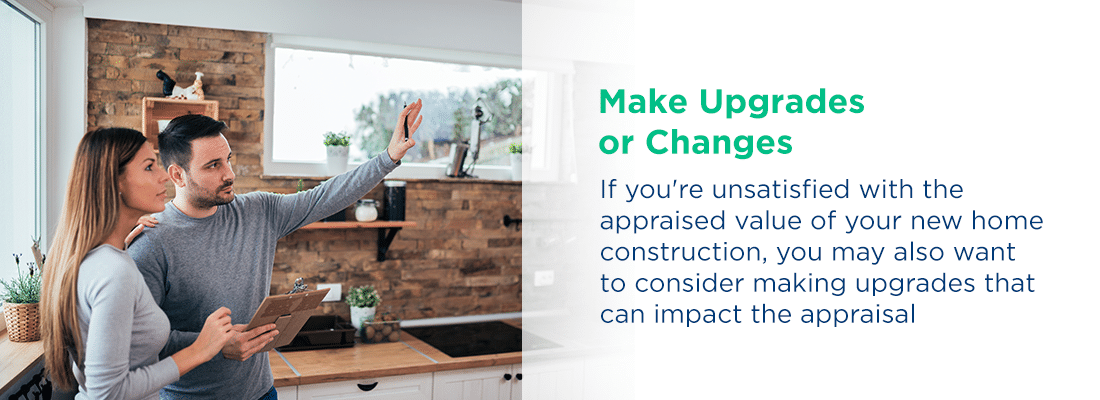

2. Make Upgrades or Changes

If you’re unsatisfied with the appraised value of your new home construction, you may also want to consider making upgrades that can impact the appraisal. Hardwood floors tend to have the most significant impact on the value of a home relative to their cost. Buyers like hardwood floors on the main level of the home, along with a hardwood staircase leading up to the second level. If it’s in your budget, you may also want to consider hardwood on the landing and hall of the second level.

Some features are low-value, high-cost items. Maybe they’re on your list of desired aspects of your home, but they will likely work against you during an appraisal. A basement will probably be on this list, as it’s essentially a concrete wall underground that contains a room or two and doesn’t add much square footage. But a basement requires excavation, plumbing and the cost of concrete, meaning it’s costly without contributing much value to the property. Another example is a wraparound porch, which may add a little extra room to your structure but doesn’t count toward the home’s total square footage.

You don’t necessarily need to give up your dream basement or wraparound porch, but you may want to discuss with your builder whether these features will be worth the hurdle you’ll face during an appraisal. Whatever upgrades you choose, research their cost-effectiveness. If you can find an upgrade that adds a lot of value at little cost, try to incorporate those changes into your home construction plans to increase the appraisal value.

After you’ve made any necessary changes for the appraisal, your appraiser will send the information on to your lender.

3. Finance Your Construction Loan

After the appraisal is completed, the lender will determine the actual amount they’re willing to lend you for your construction project. The loan you’ll receive will be the lesser amount of:

- The maximum amount you are qualified to borrow

- 80% of your home’s appraised value

Maybe you’ve been approved for a $200,000 loan. If the value of your home is appraised to be $250,000, 80% of that is $200,000. Because you’ve been approved for a $200,000 loan, you’ll receive that full amount from your lender. However, if your home is appraised to be $225,000, 80% of that is $180,000, and that is the amount you will receive from your lender.

You may choose a combination loan, also known as a construction-to-permanent loan, which is when a construction loan is combined with a long-term loan. Because construction loans are short-term loans, you may want a loan that begins after construction on your new home is completed.

During the construction period, you will pay interest only. When this construction loan period is complete, your loan will then convert to an amortized loan.

4. Underwriting for Construction Loans

For a construction-only loan, a lender will generally require a take-out loan as the source of repayment from another lender. This second lender will provide the loan to the borrower once construction is complete. The lender for a construction-only loan will be less concerned with the borrower’s qualifications, but they will review the builder’s experience and the construction contract.

For construction-permanent loans, lenders will put more emphasis on a borrower’s qualifications, such as their credit, assets and income ratios.

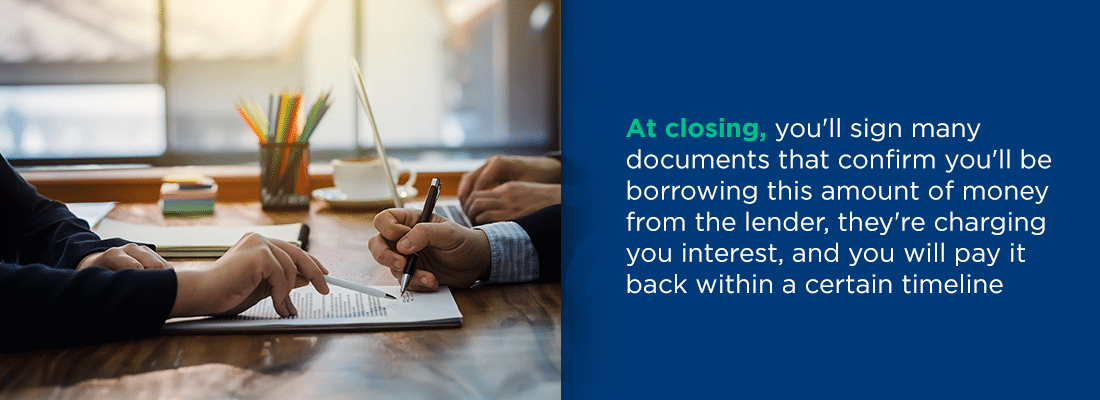

5. Closing

To close on your construction loan, you’ll need:

- The clean title for your land

- The appraisal report

- The final underwriting

At closing, you’ll sign many documents that confirm you’ll be borrowing this amount of money from the lender, they’re charging you interest, and you will pay it back within a certain timeline. Lenders use a deed of trust and a promissory note for construction loans, along with a building loan agreement that includes:

- How the loan will be disbursed

- When the loan will be disbursed

- The conditions to the disbursements, such as title endorsements, percentage of completion, inspections and lien releases

When you’re ready to finance your new construction home, Assurance Financial is here.

[download_section]

Finance Your New Home Construction With Assurance Financial

Whether you or the builder finance the home, the process is meant to be as seamless and intuitive as possible. Some people may not know the steps to take or the questions to ask, but that’s why we’re here.

Financing and constructing your dream home should be one of the most exciting times of your life. At Assurance Financial, we want to help you make this step in your journey memorable and easy. We’re an independent lender, and we specialize in making homeownership dreams come true. When you work with us, you’ll receive end-to-end processing under one roof.

Ready to finance your new home construction? Contact one of our loan officers today to find out how we can help you finance your next construction build!